The MP proposes the introduction of risk negotiation window of up to 6 per cent above the lending cap for SMEs and unsecured Individual customers.

The MP proposes the introduction of risk negotiation window of up to 6 per cent above the lending cap for SMEs and unsecured Individual customers.

5The digital financial services provider Branch Kenya announced their largest commercial paper issuance to date, raising Ksh500 million. It also plans to set up shop in India in 2019

By Brian Yatich

Conversations around insurance products for small business owners and individuals in Kenya is often met with half-hearted responses. Many view insurance covers as unnecessary expense. Others see it as a luxury instead of a necessity. Insurance penetration in Kenya is below 3 per cent with only 20 per cent of Kenyans having some form of cover.

Insurance providers have over the years been devising ways to further grow insurance services in the country. Microinsurance has slowly emerged as a possible way of roping in families with low income. One of the key areas, insurance companies are looking to rope in this population is through technology.

Technology has brought out a different side of insurance, making it an easier and quicker process for people and businesses to choose from, presenting a variety of products either through online or through mobile phones Via Smartphones Apps or USSD Codes.

One such insurer, seeking to capitalize on this prospective sector is Bluewave Insurance Company. The micro-insurance entity focuses on mid and lower income bracket.

“Around 1.2 billion Africans do not have immediate access to insurance products. Every day insurable risks such as health slowly lead people into poverty. We seek to change that,” says Adelaide Odhiambo, the Founder Bluewave Insurance.

Bluewave uses research, innovation, and technology to come up with insurance products that resonate well with the low-end market making insurance simple and easy giving their clients the right options to choose better.

With a robust micro insurance platform, Odhiambo alludes that they design microinsurance products that work for the local mwananchi which enables easy, affordable access to insurance.

Odhiambo who has over 13 years working for top insurance companies such as Jubilee Insurance, APA insurance and Liberty Insurance, has grasped massive skillset and experience in designing, developing and managing both conventional and microinsurance products. “Our objective from day one has always been people-centric, how will this influence and create an impact on the society,” she says.

The firm’s offering range from micro-insurance offerings covers motor, health and life covers. Bluewave, through its core product Imarisha Jamii applies its technology capabilities to improve clients’ enrolment, product-service and processing claims through a digital platform.

Using USSD-based platform, users can compare and choose from a range of plans across top insurance companies where they will be allowed to understand the key features and be able to buy policies instantly and safely.

“Imarisha Jamii has opened opportunities for anyone between the ages of 18 and 65 years old irrespective of their pre-existing medical conditions covering hospital expenses, disability and death at a cost of KShs. 20 weekly.”

Ms Odhiambo adds that Bluewave has made the option simple for any user to access insurance even for clients who are using the basic feature phone at a click of a button and in the comfort of their homes.

Users simply dial the *643# and then select the Imarisha Jamii option. They enter their financial output followed by amount. Users have the option of paying either on a weekly or a monthly premium. Payments are made over mobile money platform M-PESA. The Insurtech firm cashes in through administration fees from every subscriber in their platform and also earns commissions from each premium they have collected.

“Through technology, Bluewave has addressed the most common customer complaints customers have. This include of delayed payment of claims, the tedious paperwork as well as having to walk in to an insurance branch to receive service,” she says.

Partnership

Licensed as an insurance intermediary and a technology company, the insurance firm uses aggregators like Mobile Network Operators (MNO’s), Banks and Microfinance Institutions to disseminate their products.

Odhiambo says is the reason that people don’t have access to insurance is perhaps the general assumption and understanding of how insurance works is another obstacle, efficiency of the process and Bluewave is demystifying those barriers as a business.

Odhiambo believes that insurance penetration will continue to rise as the country is fast adopting fintech solutions. “People are becoming more and more aware about their financial needs as well as how to secure themselves.”

A sign that Bluewave is creating an impact in the market, the startup was named the best startup in Nairobi – representing Kenya and earning a place at the global SeedStars World competition final and the chance to pitch for US$1 million in equity investment.

“I believe we have a strong product we believe will change how our continent addresses risks. Africa needs to rise and solve its own problems and rely less on the western world,” she says.

Looking into the future Bluewave is intending to grow significantly with an ambition to cut across the insurance sector with an ambition to grow in over 10 markets by 2030, “We are aggressively looking for investors who can propel us, we believe that we can create a disruption in Africa by tapping at the bottom of the pyramid,”

As a final word of advice for upcoming entrepreneurs and startup driving companies, Adelaide Odhiambo encourages that whichever gender you are if you have a strong passion and purpose beyond any financial compensation in changing people’s lives, go for it!

Habil Olaka sits calmly at his corner office at the thirteenth floor of International House along Nairobi’s Mama Ngina Street. Dressed in a navy blue suit, white shirt and a maroon tie, he speaks thoughtfully. Every so often pausing to find the right phrase. In person, Olaka is very calm and courteous and exuding a confident air that is helped by décor and paintings in his office. Yet in his mind must be spin of thoughts and emotions, following a series of events in Kenyan business and politics arena that made the last three years ‘difficult’ for him.

As the CEO of Kenya’s bankers umbrella body the Kenya Bankers Association (KBA), the eight years he has been at the helm, he has had various responsibilities including lobbying on behalf of the banking industry and ensuring that banking practice and stability is at par with customer expectations.

The last three years has been a test of resilience and credibility. Kenya’s banking sector was facing a defining moment that threatened its catalytic role as a key driver of the country’s economic growth. Banks were struggling with a combination of issues around capital, liquidity and profitability.

More than 20 bank branches closed in 2017 alone and over 1500 bank staff laid off as banks moved to check their operational costs. The collapse of three mid-sized banks in 2015 and 2016 also showed an emerging pattern of systematic challenges, questionable governance practices, feeble supervision and widespread fraud in the industry.

In addition to these challenges, the amendment of the Banking Act in 2016 that led to the introduction of rate caps also hit the industry. The law saw lending rates capped at four percentage points above the Central Bank Rate (CBR). The deposit rate was set at least be 70 per cent of the lending rate. The move was seen as an effort by the government to curb the runaway interest rates prevailing in the market then.

For Olaka, his main task has been, to first reinstate consumer confidence in the industry. “The collapse of the three banks was brought about by poor governance and widespread fraud and that hurt the confidence of our customers. Key priority was to restore sanity in the industry.”

Habil Olaka, CEO, Kenya Bankers Association.

KBA, in a bid to restore sanity and confidence, signed up to a self-regulatory framework and conduct standards in 2016. “We wanted to ensure that the member banks work towards a shared object that led to the stability of the sector. Self-regulation is among the best ways we felt would boost corporate governance standards.”

The framework led to the introduction of punitive measures against member banks that did not adhere to the self-regulation set.

Olaka who prior to joining KBA, was in charge of portfolio quality and growth at East African Development Bank in Uganda, says that the efforts towards self-regulation are slowly bearing fruits, albeit at small scale. “Self-regulation consisted of being attentive about the interest of the sector stakeholders by addressing concerns before they become crisis.”

Sitting on Olaka’s in-tray is getting a workable formula on the interest rate capping that is favorable to the banks and the consumers. He mentions that the law had two functions. First was to stimulate a saving culture among Kenyans by placing a floor on deposits where banks could pay a minimum deposit rate on interest earning accounts. Secondly, it was meant to make lending cheaper and affordable for the common mwananchi.

However, Olaka says the law has not been effective. In fact it has led to greater challenges for the banks and customers. “Currently, market segments deemed to be high risk cannot easily access loans. This has led to credit rationing where lenders are unwilling to advance additional funds to borrowers at the prevailing market interest rate. The risk adjusted return on government debt is higher making it more attractive to lend to government than the riskier borrowers.”

KBA has been lobbying the government to scrap the rate cap law and already, the government is looking to revise the rate cap law. Olaka says the critical thing is that there is now a body of evidence clearly showing the intended positive impact on the economy is not being achieved and to the contrary it is dragging down the output growth rate of the economy.

Away from the hurdles, one of Olaka’s greatest achievement has been the establishment of Pesalink, the money transfer platform that allows for interbank transfers from one person to another on all banks retail payment channels.

Olaka who started his career at audit firm Price Water-house Coopers in the audit and business advisory services division, says the idea was conceived after member banks realized that they were losing close to KSh2.3 billion to telcos through mobile money transfer services.

Pesalink, offered by KBA’s subsidiary – Integrated Payment Services Limited (IPSL) – handles person to person transfer from as allow as KSh10 to Ksh999,999. In its first five months, the platform moved KSh8 billion.

In addition to Pesalink, Olaka is also credited for overseeing the roll-out of a Cheque Truncation System (CTS) introduced in 2011. The system allows banks to electronically clear cheques eliminating the burden of physically carrying documents to the clearing house as well as eliminating fraud in the industry. Previously, the longest cheque clearing period for upcountry cheques would take ten days. This has been reduced to two days.

As the CEO of the bankers lobby group in Kenya, he continues to champion for the formation of East Africa Bankers Association. This body he says, will perform some of the function bankers associations do at a national level but now at the regional level.

“We want to engage all the stakeholders such as the regional Customs Union, EALA among others in a bid to replicate what banker’s lobby organizations are doing on the national level to regional level. We see that as a way to support seamless operation of our members.”

Olaka however laments that despite the gain and development of the financial sector, Kenya’s domestic savings are still low. One of the main reasons he cites is that most Kenyans do not have enough income to consume and save.

“This is an opportunity for banks. There is demand for credit and most of the demand is met by informal sources. Banks should extend credit offerings to the customers currently accessing credit in the informal sector.”

Since joining KBA in 2010, Olaka says he continues to remain challenged and invigorated at all times. Kenya’s financial sector is well developed with over 45 registered banks. The banking as a sub sector contributed more than 60 per cent of total assets in the financial sector between January 2016 to March 2017 according to a report by research firm, Research and Markets.

“But we always have to keep an eye on the policy direction concerning the sector,” he says. He notes that in Kenya, legislation can change anytime and that brings the risks of doing away with the progress the sector has already made over the years.

“We need to engage policy makers and propose alternatives,” he concludes.

Banks have been slow to evolve, and that has created an opportunity for fintech start-ups to take up a slice of their market share.

Username Investment CEO Reuben Kimani has urged the Government to consider Inclusionary Zoning as part of their strategy to offer affordable homes to all Kenyans.

The CEO spoke during the 26th Kenyans Homes Expo, where Username scooped the 1st Prize as the best Land Investment Company, stated that it was time the Kenyan Government considered borrowing housing ideas from states which have been successful in ending their housing crises.

“It is possible to borrow from Maryland’s Inclusionary Zoning model, which has helped the state reduce homelessness to less than 3,000 people. To make affordable housing, which is part of the Big Four Agenda a reality, policymakers will have to enact a Moderately Priced Dwelling Unit Program, which would require developers of mass housing units to incorporate a percentage of low-cost housing in their projects.”

Reuben was referring to a 1974 housing law that was passed by the County of Montgomery, in Maryland, where builders asking for permits, site plan approvals, and sub-divisional approvals to create more than 50 housing units, would have to ensure 15 percent of the units were low-cost.

“To make this plan attractive to private developers, the government should consider incentives such as density bonuses, lower land rates, tax relief, and provision of alternative low-cost building materials in addition to the buy-back proposal made by Housing Principal Secretary, Charles Mwaura. If the Housing Ministry assures developers that they will ease their construction cost, and also buy back the units that do not sell after construction, more people in the private sector will be willing to partner with the government in making affordable housing a reality.”

Reuben was addressing the Kenyan housing crisis. The current housing shortage in the country stands at 2 million units. The proposed housing agenda is set to create 500,000 low-income housing units by 2022, which still leaves a deficit of one and a half million housing units.

“Other Countries have found ways of getting private developers involved in solving the housing crisis for low-income earners. This has benefitted them in eliminating informal settlements (slums), ending homelessness and creating communities which are income integrated. Of course, there will be the challenge of high-income earners wanting to take up these units, but lawmakers can have laws enacted restricting the income gap which one needs to occupy in order to be eligible for the low-income units. We need to define low income by looking at the median household salary earned in each Kenyan town and having households which fall below this threshold getting these units.”

Addressing the competition which has been going on between the NHC and the private sector in the provision of housing, Reuben stated that it was time the two sectors came together and created a workable partnership which will result in low-income Kenyans being able to afford homes. He stated that if the government would offer infrastructure such as access roads, electricity, clean drinking water and fast approval of construction permits, developing mass housing would become achievable.

“Most of the houses being constructed by private developers only benefit middle and high-income earners. To make Affordable Living a reality for all Kenyans, the Government has to partner with private developers.”

The Kenyan Homes Expo provides a platform for Kenyans to access Real Estate investment opportunities. The expo makes it possible for property buyers to interact with realtors, construction contractors and developers, thus demystifying the real estate industry. This year’s first expo, whose theme was Affordable Living, was held between the 12th and 15th of April.

The rise of technology has allowed fintech companies to offer alternative to traditional lenders. Now this firm wants to offer credit to everyone regardless of their status

Like many others, Mary Wafula a small scale trader in Nairobi’s Kenyatta market, struggles with economic slump, growing supplier pricing as well as access to finance to sustain or even grow her business. For small scale traders like Wafula who have very little or no savings, rainy days are all about borrowing money from friends or lending institutions such as banks or credit unions.

But, banks and credit unions have been reluctant to approve any loans for small businesses even those that are considered stable. Their main argument has been that such businesses are risky and often don’t offer many returns.

The reluctance to offer loans to small business or personal loans by banks and credit unions has seen a number of fintech companies come in to save the situation.

Buoyed by the growing mobile and internet penetration, fintech companies are developing products geared towards providing digital loans to the lower cadre population. One such company is Okolea International Limited.

Okolea, is a finance company offering digital loans, money transfer, digital payment and accounting software. According to the companies CEO, Peter Muraya, the company’s goal is to leverage on existing and emerging technologies like artificial intelligence and virtual reality to power innovative financial solutions and improve the day to day lives of people.

“Our goal is to offer loans to everyone without prejudice. We believe no one should be discriminated against regardless of their social class.”

Digital lending products have been growing in popularity over the last few years. They have been known to offer smaller amounts of loans compared to micro-finance institutions.

Customers accessing higher amounts mostly invest into business while those qualifying for smaller loans often spend on consumption, emergencies and recurring expenses such as rent.

Peter Muraya CEO, Okolea International Limited

“One of the key things we have been focusing on has been quick turnaround time. The ability to get loans instantly without documentation at any time is what Okolea appealing to the market.”

For one to qualify for Okolea instant loan, all they have to do according to Muraya, is to download the app on android play store. Once, you have downloaded, you pay facilitation fee of KSh100 to access loans. The facilitation fee according to Muraya is meant to enable the company carry out a due diligence process and check applicants credit worthiness.

“This amount is to enable us conduct a background check on the borrower’s details and status from the Credit Reference Bureau (CRB).” Once the process is complete, the borrowers can access as little as Ksh150 and a maximum of KSh100, 000. Loan limit increases with the applicant’s ability to pay previous loan.

According to Muraya, the company like most digital credit companies, relies on mobile based data such as users M-Pesa transaction records to determine their credit score and loan amount.

The annual percentage range from 20 to five per cent based on the repayment period for the borrowers. Repayment period is within a month.

Those that default on their loans are blacklisted by CRB and locked out from further accessing loans. This does not only apply to loans from Okolea but other digital credit companies. Research by Microsave an international financial inclusion firm show that about 2.7 million Kenyans have been listed in the last three years. Out of these over 400,000 have been listed for amounts less than USD2.

Since inception, Okolea has been able to disburse over 500, 000 loans to its 80,000 registered members. The average amount of loan according to Muraya is KSh1200 though this figure could change in the future.

Muraya says the busiest months for the lender is during the months of January and February. “During this time people are looking for money to take their children to school after spending most of their cash on Christmas holiday. “

Kenya has more than 20 digital credit offerings with the number growing every day. This Muraya says is fueled by a growing demand for instant loans as well as the increasing popularity of mobile money transfer services.

Mshwari is currently the most popular providing both savings and loans through M-Pesa platform. Others include California backed digital lender Branch, Equitel, Tala and Saida. A growing number of loans issued with Mshwari at 63million, KCB Mpesa at 4.1million and Equitel at 3.6million.

Similar to Okolea, these apps allow users to download the app then link it with their social media accounts. The app the uses algorithms to analyse data from the user’s handset to determine their credit score.

Industry data show that 90 per cent of loans in Kenya are currently disbursed via mobile phones. Data from the Central Bank of Kenya indicate the volume of cash moved through mobile money transfer platforms in 2016 grew by a fifth to cross the KSh3 trillion mark.

Though these services have offered a solution to one of the teething problems to the common man. They have not been without challenges.

The default rates are high, says Muraya. “Most people fail to pay their loans out of ignorance, some see the loans as too little for lenders to follow up.”

There are also cases of multiple borrowing. Over time with the growing number of products and services, it has been difficult to know how many other loans borrowers have taken. This means borrowers taking more credit than they can manage. It is common for borrowers to take up a loan to pay another. This creates a debt cycle that in the end increases their default rate.

For Muraya and his team, the target is now set on growing the company’s market share. This he says will be through offering products that resonate with the market demands and trends.

Retirement schemes’ equity allocation increased over the quarter ending 30 June 2017. This was mainly caused by the rally in the stock market over the period.

The Zamara Consulting Actuaries Schemes Survey (Z – CASS) for the second quarter of 2017 shows that the allocation of equity investments increased to 21.5 per cent from 19.1 per cent in the first quarter as prices of the held investments increased.

“The Nairobi Securities Exchange (NSE) has rallied since April of this year mainly driven by Banking Stocks delivering profits, strong sustained performance from Safaricom which led to increased local and foreign investor confidence. The offshore asset class also performed well over the 12 month period. Although following the results of the supreme court judgement nullifying the election results on 1 September, the stock market took a plunge, ”said Zamara Group Chief Executive Officer Sundeep Raichura.

Fixed income assets accounted for 72.9 per cent of the average pension fund allocation followed by property at 4.3 per cent and offshore at 1.3 per cent.

The Z-CASS Survey additionally showed that participating schemes had a median return of 14.3 per cent over a one-year period and a 9.4 per cent return over a three-year period. Schemes in Kenya have varying risk profiles, the survey classifies the schemes in to three categories – Conservative, Moderate and Aggressive. During the 12 month period, schemes with moderate risk had the highest median performance and conservative schemes had the highest 3 year median performance.

Offshore investments, despite the low asset allocation, had the highest median return over a one-year period at 22.6 per cent followed by fixed income at 15.2 per cent and equity at 12.5 per cent.

Fixed income assets recorded the highest return over a three-year period at 12.9 per cent, followed by offshore investments at 10.1 per cent and equities at 1.7 per cent.

At least 382 Schemes were covered in the in the Z – CASS Survey in the second quarter of 2017 and the assets under management covered by the survey were at Ksh655 billion.

The Z- Cass Survey enables trustees to compare the performance of their retirement scheme relative to their peers within the broader retirement scheme industry.

Diversified investments company, FEP Holdings Ltd has recorded an 87 percent reduction in consolidated loss before tax for the financial year ending December 2016, moving from Ksh866 million in 2015 to Ksh108 million in 2016.

The company announced a profit after tax of Ksh106 million for 2016 compared to a loss after tax of Ksh905 million in 2015 due to a favourable tax position.

Speaking when he released the financial results, Maurice Korir, the FEP Holdings Chief Executive Officer said the company’s performance was buoyed by prudent management of operating costs and strong results from its real estate and microlending units.

“We have had improved business efficiency across the board owing to operational restructuring and better internal controls after the installation of a Sage Evolution Enterprise Resource Planning (ERP) system. Our operating expenses have reduced by 16 percent,” said Mr Korir.

The Group’s gross margin excluding interest on short-term deposits improved from 26 percent in 2015 to 34 percent in 2016. Since FEP Holdings embarked on a turnaround programme in the last quarter of 2014, the company has been cutting back on administrative costs by reducing the number of regional offices and adopting technological innovations across the business units.

Fountain Credit Services Limited (FCSL), a microfinance subsidiary of FEP Holdings has introduced Instaloan, a mobile lending platform that helps disburse loans faster and more cost effectively.

“We introduced Instaloan after acquiring a robust IT system dubbed IMAB that has made it easier to access data necessary for the disbursement of loans at the click of a button. This has helped us reduce our physical branch presence and the attendant costs that come with it”, said Mr Korir.

Improved sales for the Group’s real estate division, Kisima Real Estate, also shored up FEP Holdings Performance. The FEP Holdings subsidiary has grown by over 400% recording Ksh106 million in sales in 2016 as compared to Ksh 21 million in 2015.

“This has largely been through progress in processing title deeds and improved customer relations through one-on-one engagement forums,” revealed Mr Korir.

The Group however registered a 24 per cent dip in revenues as some of the strategic business units did not realize the projected performance targets. “Some project under Fountain Technologies Ltd (FTL) are still ongoing and there is over Ksh1 billion which we will invoice across 2017 and 2018,” added the CEO.

Last year, FTL secured a tender to implement a Ksh 1Bn energy infrastructure project for Rural Electrification Authority amongst other projects.

“For us to post better results in 2017, we need to recapitalize some of our subsidiaries as well as the holding company. We had a rights issue which was undersubscribed, having raised Ksh120 million against a target of Ksh2.6 billion,” revealed Mr Korir.

The company has already identified a strategic investor for Fountain Technologies and will appoint an advisory firm to raise external capital for the holding company.

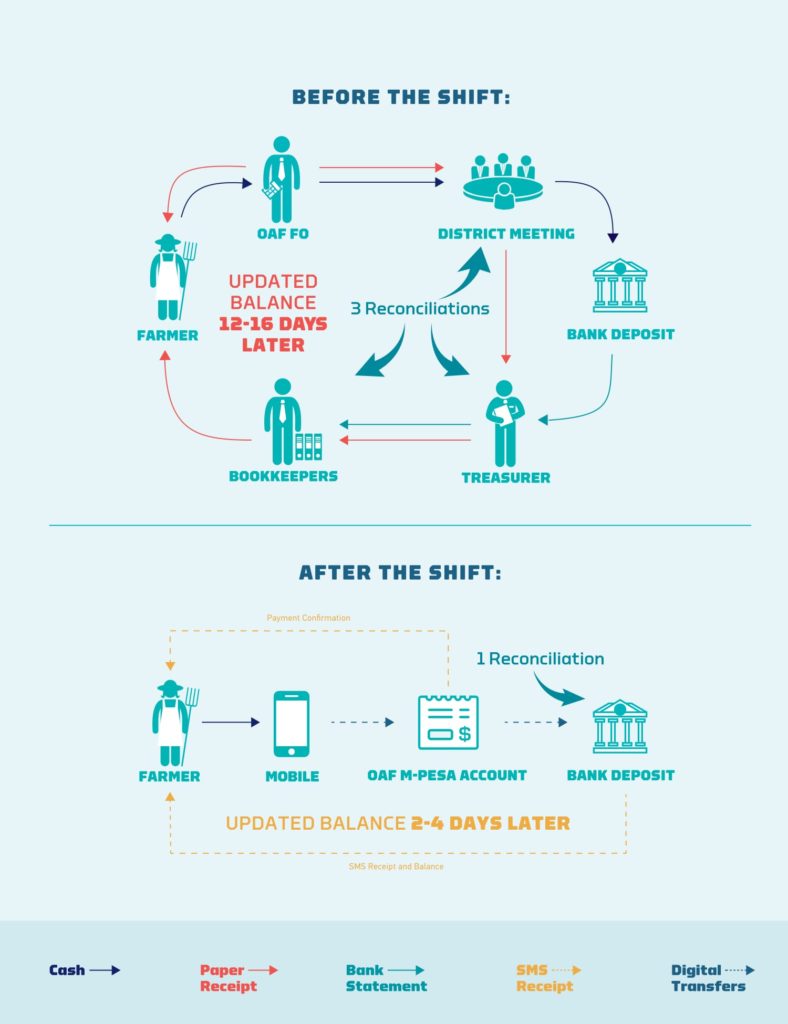

Digitization of payments has helped farmers in Kenya boost their income and combat poverty, a new case study by UN based Better Than Cash Alliance has shown. The study which focused on One Acre Fund an agricultural NGO, revealed that digitization had helped boost transparency and efficiency in the payment system. As a result, this drove economic opportunity and financial inclusion for thousand of smallholder farmers and their families.

One Acre Fund, digitized its loan repayment enabling farmers to easily make loan repayments via mobile money instead of cash. This helped reduce the uncertainty, inefficiency, insecurity and high costs previously caused by cash transactions.

One Acre Fund can now reach more farmers with greater reliability, and staff can spend almost half as much time collecting payments in cash. Inn addition they can use the extra time to help farmers increase their incomes through training and educational programs.

According to the study, One Acre Fund’s package of services, including training and inputs like seed and fertilizer, the average farmer participating in the program earned nearly 50 percent more than peer farmers who do not participate.

“We’re excited to be working at the forefront of this technology in the smallholder agriculture lending sector. In our experience, farmers were empowered to thrive in these communities. Clients receive immediate confirmation of payments as they happen, enabling them to better manage their businesses and family finances,” said Mike Warmington, the Director of Microfinance Partnerships at One Acre Fund.

“For companies and nonprofit organizations who want to work in rural Africa, this success story is a must-read,” said Oswell Kahonde, Africa Regional Lead at the Better Than Cash Alliance.

“Digital payments are essential to building sustainable business models and creating long-term impact. By enabling smallholder farmers to make and receive payments digitally, we are creating transparency and accountability which translates to numerous benefits and empowers people to take control of their finances.”

Key Highlights from the study:

Click here to download the case study http://APO.af/v5Wxdm